Are robo-advisors worth your money? With automated investing platforms gaining popularity, many investors are turning to digital solutions for portfolio management. Robo-advisors use algorithms and financial data to build and manage investment portfolios with minimal human intervention. While they offer convenience and low fees, they may not suit every investor’s needs. Understanding the pros and cons of robo-advisors is essential before committing your hard-earned capital.

What Are Robo-Advisors?

Robo-advisors are digital platforms that provide automated, algorithm-driven financial planning services with little to no human supervision. They typically assess your risk tolerance, financial goals, and time horizon through an online questionnaire. Based on this data, they allocate your investments across diversified portfolios—often using low-cost index funds or ETFs.

Popular robo-advisors like Betterment, Wealthfront, and Vanguard Digital Advisor have made investing more accessible. They’re especially appealing to beginners, passive investors, and those seeking cost-effective alternatives to traditional financial advisors.

Pros of Robo-Advisors

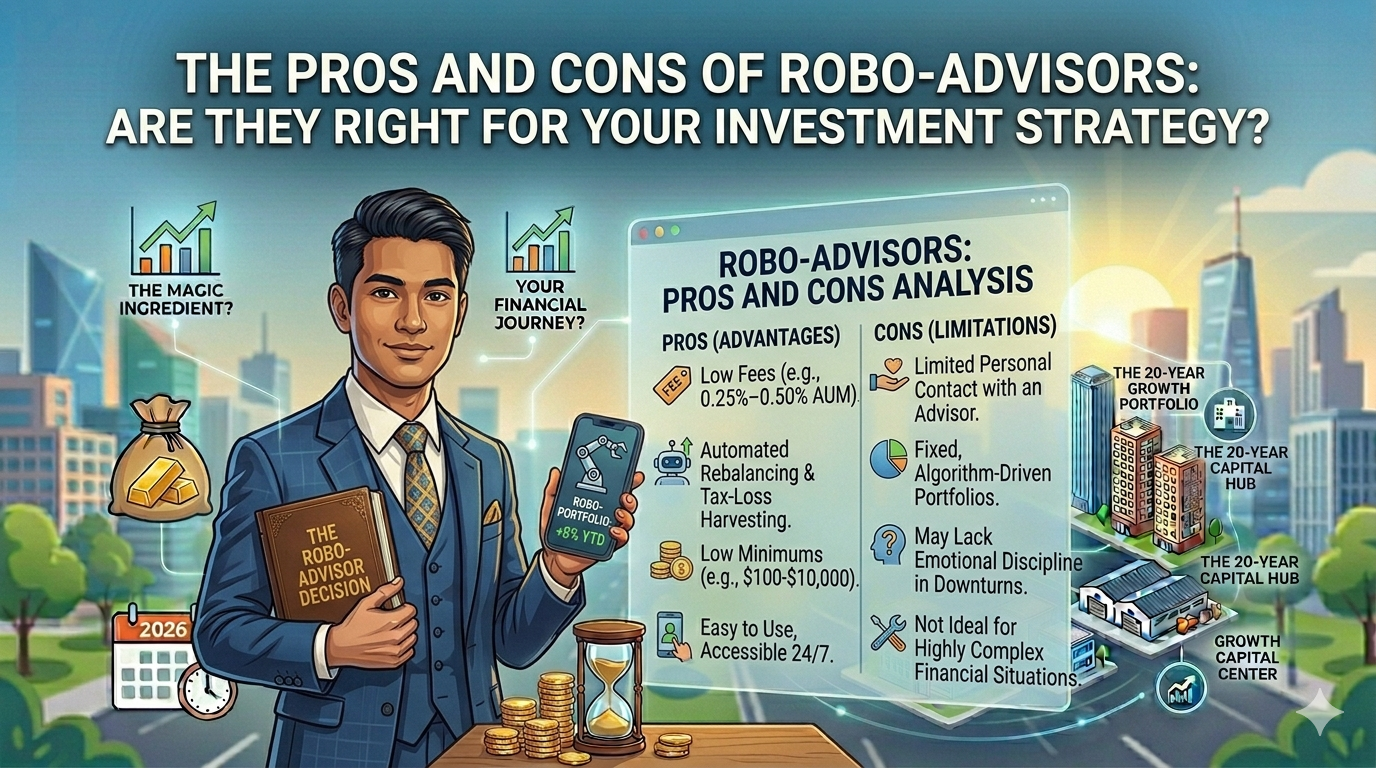

1. Low Fees and Cost Efficiency

One of the biggest advantages of robo-advisors is their affordability. Traditional financial advisors often charge 1% or more in annual management fees. In contrast, most robo-advisors charge between 0.25% and 0.50%, making them a budget-friendly option.

Lower fees mean more of your money stays invested, compounding over time. For long-term investors, even small fee differences can significantly impact final portfolio value.

2. Accessibility and Ease of Use

Robo-advisors are designed for simplicity. You can open an account in minutes, often with low or no minimum investment requirements. The user-friendly interfaces guide you through setup, risk assessment, and goal tracking.

This accessibility removes barriers for new investors who may feel intimidated by traditional wealth management services. Whether you’re saving for retirement or building a college fund, robo-advisors make it easy to get started.

3. Automated Portfolio Management

Once your account is set up, the robo-advisor handles everything—rebalancing, dividend reinvestment, and tax-loss harvesting (in some cases). This automation saves time and reduces the emotional decision-making that can derail investment performance.

Tax-loss harvesting, for example, automatically sells losing investments to offset gains, potentially lowering your tax bill. This feature is typically found in premium-tier robo-advisor plans.

4. Diversification and Risk Management

Robo-advisors build diversified portfolios based on modern portfolio theory. By spreading investments across asset classes—such as stocks, bonds, and international funds—they help reduce risk.

The algorithms adjust your asset allocation as your goals or market conditions change, ensuring your portfolio stays aligned with your risk profile.

Cons of Robo-Advisors

1. Limited Personalization and Human Touch

While robo-advisors excel at automation, they lack the personal insight of a human financial advisor. They can’t discuss complex life events—like inheritance, divorce, or career changes—that may require tailored advice.

For investors with unique financial situations, such as business owners or those with multiple income streams, a robo-advisor may fall short in providing holistic guidance.

2. One-Size-Fits-All Approach

Most robo-advisors rely on standardized questionnaires to assess risk tolerance. However, these tools may not capture the full picture of your financial behavior or emotional response to market volatility.

As a result, the recommended portfolios can feel generic. Investors seeking niche strategies—like ESG investing or sector-specific allocations—may find limited customization options.

3. No Active Management or Market Timing

Robo-advisors follow passive investment strategies, meaning they don’t attempt to beat the market. While this reduces risk and cost, it also means you won’t benefit from active management during volatile periods.

During market downturns, a human advisor might recommend defensive moves or alternative assets. Robo-advisors, however, stick to their algorithm, which could lead to slower reactions in fast-changing environments.

4. Limited Customer Support

Although many robo-advisors offer email or chat support, access to live financial advisors is often restricted to higher-tier accounts. If you have urgent questions or need clarification, waiting for a response can be frustrating.

This lack of immediate, personalized support may deter investors who value direct communication.

Who Should Use Robo-Advisors?

Robo-advisors are ideal for:

- Beginner investors with straightforward financial goals

- Passive investors who prefer a “set it and forget it” approach

- Cost-conscious individuals seeking low-fee investment options

- Those with smaller portfolios who don’t require complex planning

They’re less suitable for high-net-worth individuals, those with intricate estate planning needs, or anyone requiring hands-on financial coaching.

Key Takeaways

- Robo-advisors offer low fees, automation, and ease of use, making them attractive for new and passive investors.

- They provide diversified portfolios and features like tax-loss harvesting, but lack personalized advice and human interaction.

- The best choice depends on your financial complexity, investment goals, and preference for automation versus human guidance.

- Hybrid models—combining robo-advisors with access to human advisors—are emerging as a balanced solution for many investors.

FAQ: Common Questions About Robo-Advisors

Are robo-advisors safe?

Yes, most reputable robo-advisors are backed by established financial institutions and are SIPC-insured (up to $500,000, including $250,000 for cash). However, like all investments, they carry market risk—your returns are not guaranteed.

Can I lose money with a robo-advisor?

Absolutely. While robo-advisors manage risk through diversification, your investments are still subject to market fluctuations. During downturns, your portfolio value may decline. The key is long-term investing and staying the course.

Do robo-advisors offer retirement accounts?

Yes. Most robo-advisors support IRAs (Traditional, Roth, and SEP), 401(k) rollovers, and taxable brokerage accounts. This makes them a convenient option for retirement planning.