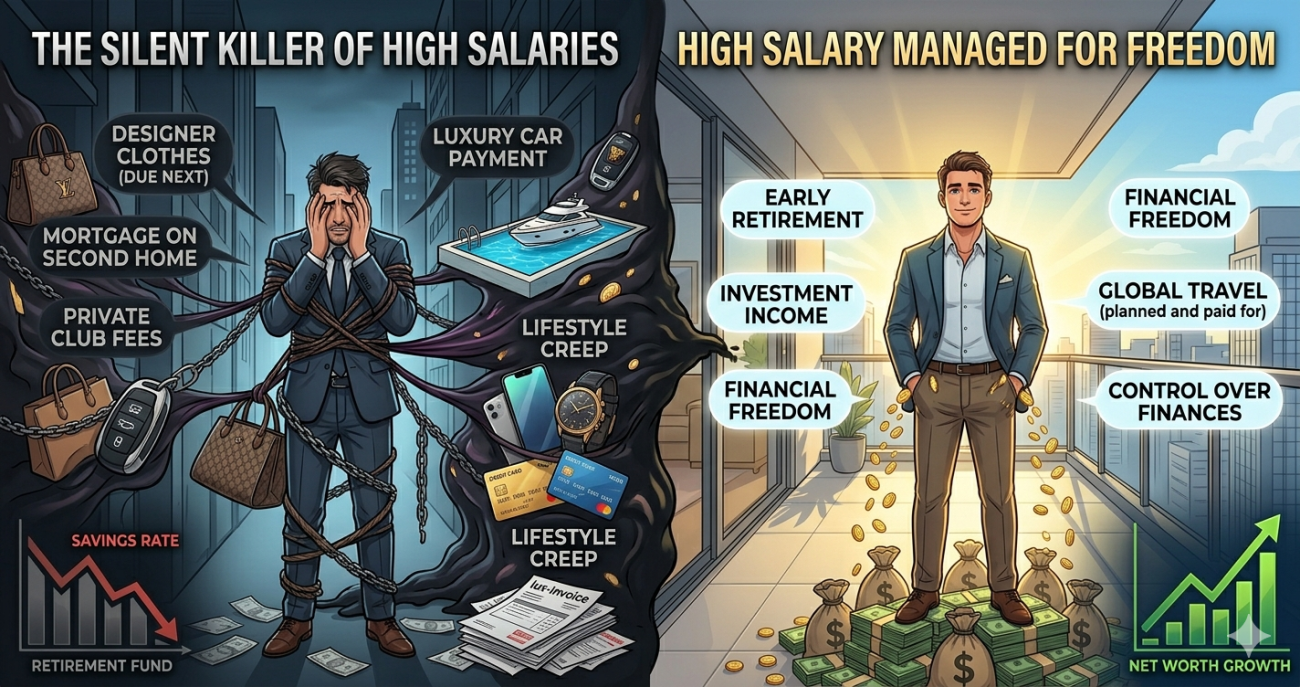

You’ve landed that six-figure salary. Congratulations. But if your bank account isn’t growing—and you’re still living paycheck to paycheck—you might be falling victim to lifestyle creep. This subtle, often invisible phenomenon quietly erodes financial progress, even among high earners. Lifestyle creep occurs when increased income leads to proportionally increased spending, leaving savings and investments stagnant. It’s the silent killer of wealth building, especially for professionals who believe earning more automatically means being richer.

Imagine earning $150,000 a year but saving less than someone making $70,000. That’s not a myth—it’s a common reality fueled by lifestyle creep. As salaries rise, so do expectations: bigger homes, newer cars, premium subscriptions, and frequent dining out. The result? A lifestyle that matches the paycheck, but not the long-term financial goals. This article dives deep into how lifestyle creep sabotages high earners, why it’s so hard to spot, and how to break free before it derails your financial future.

What Is Lifestyle Creep—And Why Does It Target Six-Figure Earners?

Lifestyle creep, also known as lifestyle inflation, happens when people increase their standard of living in response to higher income—without a corresponding increase in savings or investments. It’s not about splurging once; it’s about making permanent upgrades to daily habits and recurring expenses.

For six-figure earners, the danger is especially high. When you’re used to a certain income level, even modest raises can trigger automatic upgrades. A $10,000 annual raise might go straight into a car payment, a larger mortgage, or more expensive vacations—instead of retirement accounts or emergency funds. Over time, these small shifts compound into a lifestyle that’s expensive to maintain, even if it doesn’t feel extravagant day to day.

Unlike sudden financial disasters, lifestyle creep is gradual. It doesn’t scream for attention. That’s what makes it so dangerous. You don’t notice the erosion until you’re financially overextended, unable to save, and unprepared for unexpected expenses.

How Lifestyle Creep Sneaks In

- Housing upgrades: Moving to a more expensive neighborhood or buying a larger home after a promotion.

- Transportation inflation: Leasing a luxury vehicle instead of keeping a reliable, paid-off car.

- Subscription stacking: Adding premium streaming, meal kits, gym memberships, and apps without evaluating necessity.

- Dining and entertainment: Eating out more frequently, traveling first-class, or attending costly events.

- Social pressure: Keeping up with peers who also earn well, leading to peer-driven spending.

These changes often feel justified. After all, you deserve to enjoy your success. But without conscious financial planning, enjoyment can quickly turn into financial fragility.

The Psychology Behind Lifestyle Creep

Lifestyle creep isn’t just about money—it’s deeply tied to psychology. Behavioral economists call this the hedonic adaptation: the tendency to return to a baseline level of happiness after positive changes, like a raise. So, that initial excitement over a higher salary fades, and you start craving the next upgrade to feel the same thrill.

There’s also the status signaling effect. High earners often equate spending with success. A luxury watch, a designer bag, or a high-end apartment can feel like proof of achievement. But these symbols don’t build wealth—they consume it.

Another factor is mental accounting: the way people treat money differently based on its source. A bonus or tax refund might feel like “free money,” leading to impulsive spending. But that mindset ignores the long-term impact of diverting funds from savings or debt repayment.

Finally, there’s the lifestyle trap: once you’re used to a certain standard of living, it’s hard to downgrade. Going from a $3,000 monthly rent to $1,500 feels like a sacrifice, even if it frees up $18,000 a year for investing.

Real-Life Examples of Lifestyle Creep in Action

Consider Sarah, a software engineer who landed a $140,000 job in San Francisco. Within a year, she upgraded her studio apartment to a two-bedroom in a trendy neighborhood, leased a Tesla, and started dining out five nights a week. She also joined a premium fitness studio and traveled internationally twice a year. Her take-home pay increased, but her savings rate dropped from 20% to 5%.

Or take Mark, a marketing director earning $160,000. After a promotion, he bought a $700,000 home with a $4,500 monthly mortgage. He justified it by saying, “I’m investing in real estate.” But he also took on a $1,200 car payment, $300 in streaming services, and $800 monthly on weekend trips. His net worth stagnated, and when he faced a medical emergency, he had to dip into credit cards.

These aren’t outliers. They’re typical of professionals who let lifestyle creep go unchecked. The irony? Many high earners live with financial stress, not because they earn too little, but because they spend too much of what they earn.

How to Spot Lifestyle Creep Before It Spots You

The first step to stopping lifestyle creep is awareness. Here are red flags to watch for:

- Your savings rate hasn’t increased despite a raise.

- You can’t remember the last time you reviewed your budget.

- You feel guilty about spending but do it anyway.

- Your monthly expenses grow faster than inflation.

- You rely on credit cards for non-emergency purchases.

- You can’t imagine cutting back on any current expense.

If any of these sound familiar, it’s time to audit your finances. Track every dollar for one month. Use apps like Mint, YNAB, or even a simple spreadsheet. You’ll likely discover spending patterns you didn’t realize were there.

Ask yourself: Would I still buy this if I earned 20% less? If the answer is no, it’s likely a lifestyle creep expense.

Breaking the Cycle: How to Stop Lifestyle Creep

Stopping lifestyle creep isn’t about deprivation—it’s about intentionality. Here’s how to take back control:

1. Automate Your Savings

The moment you get a raise, increase your savings rate—not your spending. Set up automatic transfers to retirement accounts, emergency funds, or investment portfolios. If the money never hits your checking account, you won’t miss it.

2. Adopt the “Pay Yourself First” Rule

Before paying bills or buying groceries, allocate a percentage of your income to savings and investments. Treat this like a non-negotiable expense. Experts recommend saving at least 15–20% of gross income, especially for high earners.

3. Use the 30-Day Rule

Before making any non-essential purchase over $200, wait 30 days. This cooling-off period helps distinguish between wants and needs. Often, the urge to buy fades.

4. Downsize Strategically

You don’t have to live in a mansion to feel successful. Consider downsizing your home, car, or subscription services. The money saved can go toward financial freedom—like paying off debt or building passive income.

5. Focus on Experiences, Not Things

Shift spending from material goods to meaningful experiences: travel, learning, time with family. These create lasting memories without inflating your lifestyle permanently.

6. Set Clear Financial Goals

Without goals, it’s easy to drift into overspending. Define what financial success looks like for you: early retirement, financial independence, starting a business. Let those goals guide your spending decisions.

Key Takeaways

- Lifestyle creep is the gradual increase in spending that matches income growth, often leaving high earners financially stagnant.

- It’s especially dangerous for six-figure earners who may confuse spending with success.

- Psychological factors like hedonic adaptation and status signaling fuel the cycle.

- Signs include stagnant savings, rising expenses, and reliance on credit.

- Combat it by automating savings, using the 30-day rule, and focusing on long-term goals.

- True wealth isn’t about how much you earn—it’s about how much you keep and grow.

FAQ

What is lifestyle creep?

Lifestyle creep is the tendency to increase spending as income rises, often leading to little or no improvement in savings or net worth. It’s common among high earners who upgrade their lifestyle without adjusting their financial habits.

Can lifestyle creep affect people who don’t earn six figures?

Absolutely. While it’s most noticeable among high earners, anyone who increases spending in response to a raise or bonus can fall victim. The principle applies at any income level.

How can I tell if I’m experiencing lifestyle creep?

Check if your savings rate has stayed the same or decreased despite higher income. Also, review whether your monthly expenses have grown faster than inflation. If you’re living paycheck to paycheck despite earning well, lifestyle creep may be the cause.

Is it bad to enjoy my salary?

Not at all. Enjoying your income is healthy and deserved. The key is balance—allocate a portion to enjoyment while prioritizing savings and financial goals. You can live well and build wealth.

Final Thoughts

Earning a six-figure salary is an achievement, but it doesn’t guarantee financial security. Without mindful money management, lifestyle creep can quietly drain your wealth, leaving you no better off than someone earning half as much. The solution isn’t to earn less—it’s to spend with purpose.

Start today. Review your budget. Identify one expense you can reduce or eliminate. Automate a savings transfer. Small, consistent actions break the cycle of lifestyle creep and pave the way to lasting financial freedom. Remember: your salary is what you earn. Your wealth is what you keep.