Struggling to balance your income, savings, and lifestyle? You’re not alone. The 50/30/20 rule offers a simple, proven framework to help beginners achieve financial balance without complex budgeting tools or spreadsheets. By dividing your after-tax income into three clear categories—needs, wants, and savings—this rule brings clarity to your spending habits and builds a foundation for long-term financial health.

What Is the 50/30/20 Rule?

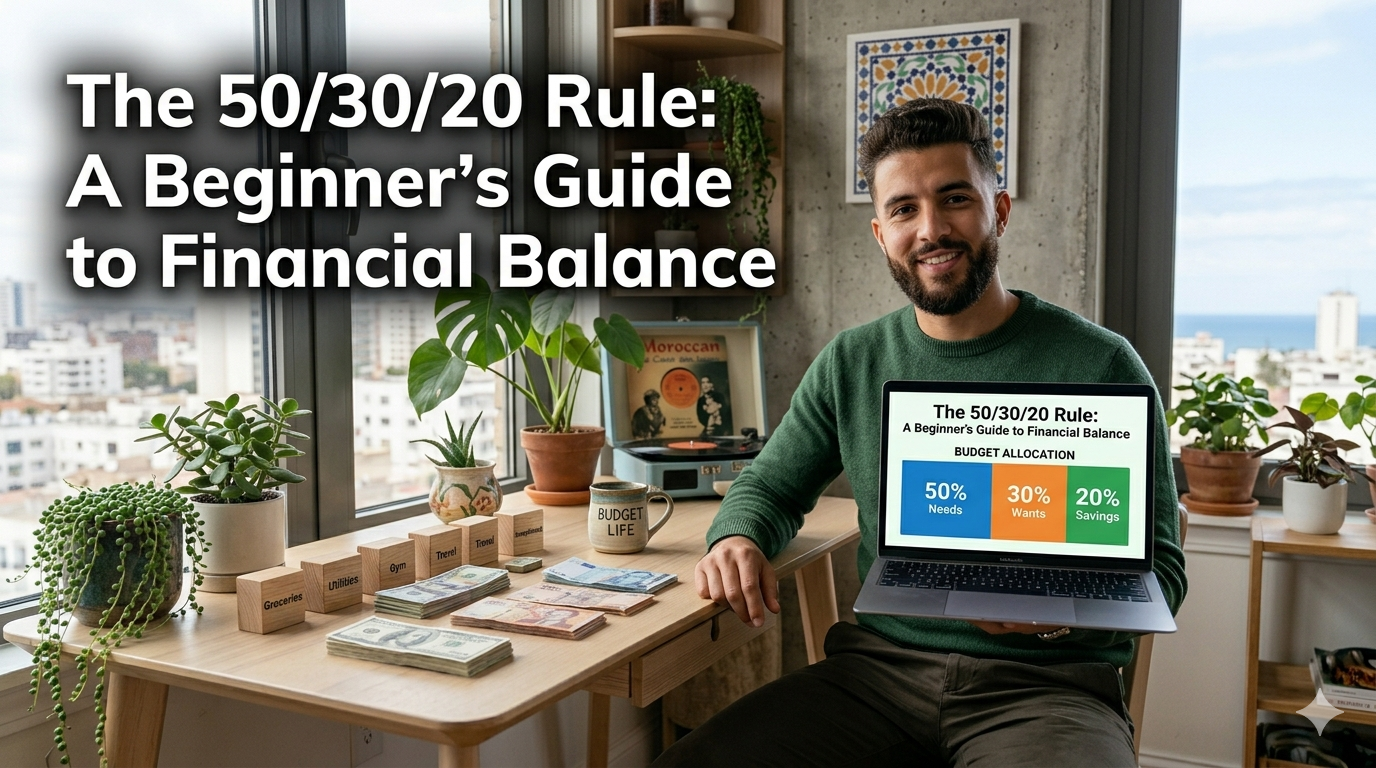

The 50/30/20 rule is a straightforward budgeting method created by U.S. Senator Elizabeth Warren. It divides your monthly take-home pay into three portions:

- 50% for Needs: Essential expenses you can’t live without, like rent, utilities, groceries, transportation, and minimum debt payments.

- 30% for Wants: Non-essential spending on lifestyle choices, such as dining out, entertainment, subscriptions, and vacations.

- 20% for Savings and Debt Repayment: Money set aside for emergency funds, retirement accounts, investments, and paying down high-interest debt.

This structure helps you prioritize financial responsibilities while still allowing room for personal enjoyment—making it ideal for those new to budgeting.

Why the 50/30/20 Rule Works for Beginners

Unlike rigid budgets that demand tracking every dollar, the 50/30/20 rule focuses on broad spending categories. This simplicity reduces overwhelm and increases the likelihood of long-term adherence. It’s especially effective for people with steady incomes who want to build financial discipline without sacrificing quality of life.

By clearly separating needs from wants, you gain better control over impulsive spending. At the same time, allocating 20% toward savings ensures you’re proactively building wealth and preparing for unexpected expenses.

How to Apply the 50/30/20 Rule Step by Step

Step 1: Calculate Your After-Tax Income

Start by determining your monthly take-home pay—the amount you receive after taxes and deductions. If your income varies, use an average of the last three to six months. This number forms the basis of your 50/30/20 budget.

Step 2: Categorize Your Expenses

Review your bank statements or use a budgeting app to list all monthly expenses. Then, sort them into the three categories:

- Needs (50%): Rent/mortgage, electricity, water, internet, groceries, insurance, car payments, and minimum credit card payments.

- Wants (30%): Streaming services, gym memberships, coffee shops, shopping, travel, and eating out.

- Savings & Debt (20%): Emergency fund contributions, retirement accounts (like a 401(k) or IRA), extra debt payments, and investments.

If you’re unsure whether an expense is a need or a want, ask: “Can I live without this?” If the answer is no, it’s a need.

Step 3: Adjust Your Spending

Compare your actual spending to the 50/30/20 targets. If you’re overspending in one category, identify areas to cut back. For example, if wants exceed 30%, reduce dining out or cancel unused subscriptions. Redirect those funds to needs or savings.

Remember, the goal isn’t perfection—it’s progress. Small, consistent adjustments lead to lasting financial balance.

Common Challenges and How to Overcome Them

Even with a clear system, sticking to the 50/30/20 rule can be tough. High-cost living areas, student loans, or irregular income may make the 50% needs category difficult to maintain.

In such cases, flexibility is key. If your rent alone consumes 40% of your income, you may need to temporarily adjust the ratios—perhaps 55/25/20—while working toward higher income or lower expenses. The rule is a guideline, not a rigid law.

Another challenge is distinguishing between wants and needs. For instance, a reliable car might be a need for commuting, but a luxury vehicle upgrade is a want. Be honest with yourself to avoid budget leaks.

Benefits of Using the 50/30/20 Rule

Adopting this rule offers several advantages:

- Simplicity: No need for complex tracking—just three categories.

- Balance: Encourages responsible spending while allowing enjoyment.

- Financial Security: Builds emergency savings and reduces debt over time.

- Mindset Shift: Promotes awareness of spending habits and financial priorities.

Over time, this approach fosters confidence in managing money and lays the groundwork for more advanced financial strategies.

Key Takeaways

- The 50/30/20 rule divides after-tax income into needs (50%), wants (30%), and savings/debt repayment (20%).

- It’s ideal for beginners seeking a simple, sustainable budgeting method.

- Start by calculating your take-home pay and categorizing expenses accurately.

- Adjust ratios as needed based on your financial situation and cost of living.

- Consistency and self-awareness are more important than perfection.

FAQ

Can I use the 50/30/20 rule if I have a low income?

Yes. While it may be challenging in high-cost areas, the rule can still guide your priorities. Focus on minimizing wants and maximizing savings, even if the percentages shift slightly. The goal is progress, not perfection.

What counts as a “need” versus a “want”?

Needs are essentials required for basic living: housing, food, healthcare, transportation, and utilities. Wants are discretionary expenses that enhance lifestyle but aren’t necessary for survival, like vacations, premium subscriptions, or designer clothing.

Should I include retirement savings in the 20%?

Absolutely. The 20% category is designed for both short-term savings (like an emergency fund) and long-term goals (like retirement). Contributing to a 401(k) or IRA counts toward this portion and helps secure your financial future.