High earners often hit the contribution limits on traditional retirement accounts—leaving thousands of dollars on the table each year. If you’re making six or seven figures and maxing out your 401(k) and IRA, you need a smarter way to grow your wealth tax-free. Enter the “Mega Backdoor Roth”—a powerful, IRS-permitted strategy that allows high-income individuals to contribute up to $46,000 extra annually into a Roth IRA through their employer-sponsored retirement plan. This isn’t a loophole; it’s a legal, underutilized tool that can dramatically accelerate your path to financial freedom.

What Exactly Is the Mega Backdoor Roth?

The Mega Backdoor Roth is a strategy that leverages a specific provision in certain 401(k) plans to convert after-tax contributions into Roth funds. Unlike the standard backdoor Roth IRA—which is limited to $7,000 per year (2024 limit)—the Mega Backdoor Roth allows significantly larger contributions, often exceeding $40,000 annually.

It works by taking advantage of IRS rules that permit after-tax contributions to 401(k) plans beyond the standard employee deferral limit ($23,000 in 2024). If your plan allows in-service withdrawals or in-plan Roth conversions, you can convert those after-tax contributions into a Roth 401(k) or Roth IRA—growing tax-free for decades.

This strategy is especially valuable for high earners who are already maxing out their pre-tax and Roth 401(k) contributions and want to maximize tax-advantaged retirement savings.

How It Differs from the Standard Backdoor Roth

- Contribution Limits: The standard backdoor Roth is capped at $7,000 (plus $1,000 catch-up if over 50). The Mega Backdoor Roth can allow over $46,000 in additional annual contributions.

- Plan Dependency: The Mega Backdoor Roth only works if your 401(k) plan permits after-tax contributions and in-service Roth conversions.

- Tax Treatment: Both strategies result in tax-free growth, but the Mega Backdoor Roth offers exponentially greater capacity for wealth accumulation.

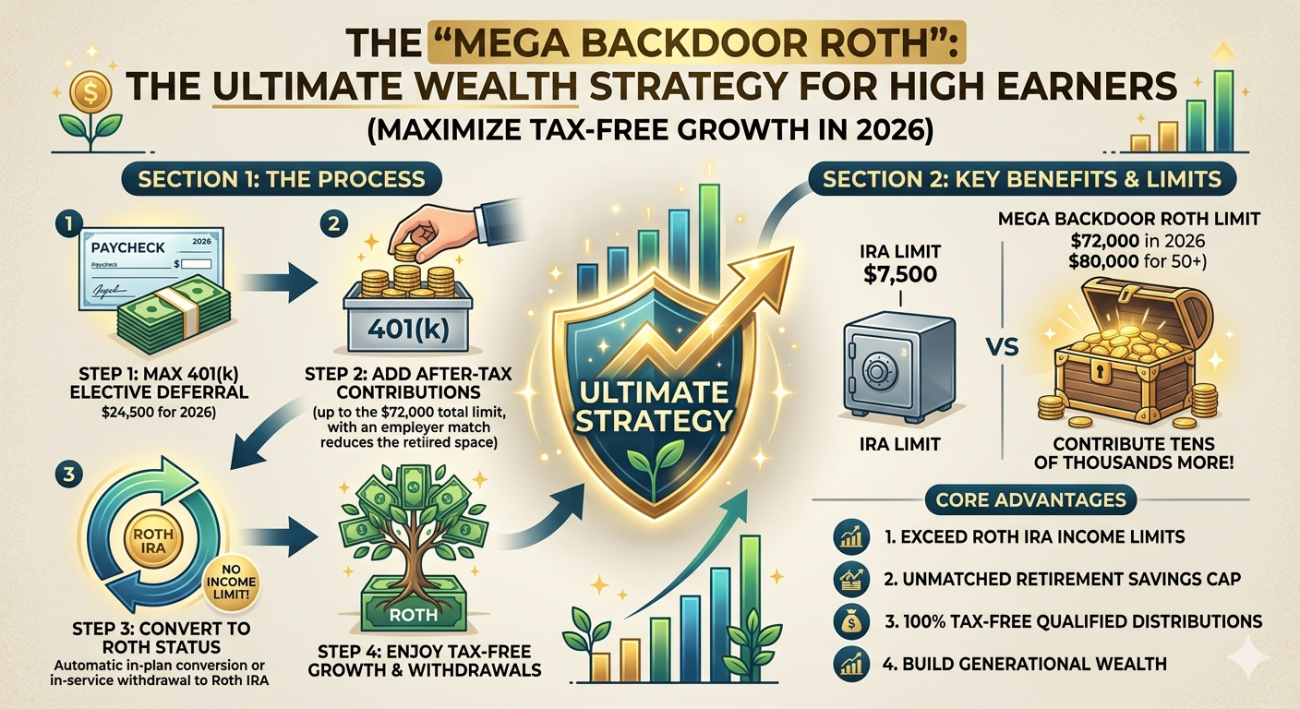

How the Mega Backdoor Roth Works: A Step-by-Step Breakdown

Executing the Mega Backdoor Roth isn’t automatic—it requires careful planning and coordination with your employer’s retirement plan. Here’s how it works in practice:

Step 1: Confirm Your Plan Allows After-Tax Contributions

Not all 401(k) plans permit after-tax contributions. You must check your Summary Plan Description (SPD) or speak with your plan administrator. If your plan only allows pre-tax or Roth deferrals, the Mega Backdoor Roth isn’t an option—unless you advocate for a plan change.

Step 2: Max Out Your Employee Deferrals

Start by contributing the maximum employee deferral amount—$23,000 in 2024 (or $30,500 if you’re 50 or older). This includes both pre-tax and Roth contributions. This step is essential because the IRS sets a total contribution limit for all employee and employer contributions combined.

Step 3: Make After-Tax Contributions

Once you’ve maxed your deferral, you can contribute additional after-tax dollars. The IRS allows total contributions (employee + employer + after-tax) up to $69,000 in 2024 (or $76,500 with catch-up). If your employer matches 5%, for example, you could contribute up to $46,000 in after-tax funds.

Step 4: Convert After-Tax Contributions to Roth

This is the critical step. You must convert your after-tax contributions into a Roth account—either within the 401(k) (if allowed) or by rolling them into a Roth IRA. This conversion is tax-free because you’ve already paid taxes on the contributions.

Step 5: Repeat Annually

The Mega Backdoor Roth isn’t a one-time move. To maximize its benefits, you must execute it every year, ideally right after each paycheck, to minimize earnings on after-tax funds (which are taxable if not converted promptly).

Why High Earners Should Care: The Tax-Free Growth Advantage

For high-income professionals—doctors, lawyers, executives, entrepreneurs—the Mega Backdoor Roth is a game-changer. It allows you to shelter massive amounts of wealth from future taxes while compounding returns tax-free.

Imagine contributing $46,000 annually for 20 years, earning a modest 7% return. That’s over $1.9 million in tax-free growth. Without this strategy, that same money would be taxed annually in a brokerage account, significantly reducing your net returns.

Additionally, Roth accounts have no required minimum distributions (RMDs), meaning you can leave the money untouched for decades—or pass it on to heirs tax-free.

Real-World Impact: A Case Study

Sarah, a 45-year-old physician earning $400,000 annually, maxes out her 401(k) and wants to save more. Her employer’s plan allows after-tax contributions and in-plan Roth conversions.

- She contributes $23,000 in Roth 401(k) deferrals.

- Her employer matches $12,000.

- She contributes $34,000 in after-tax funds.

- She converts the $34,000 to Roth immediately.

Total tax-advantaged savings: $69,000. Over 20 years, this could grow to over $2.8 million—tax-free.

Key Requirements and Pitfalls to Avoid

While powerful, the Mega Backdoor Roth isn’t without risks. Here’s what you need to know:

1. Your 401(k) Plan Must Allow It

Not all plans permit after-tax contributions or in-service Roth conversions. If yours doesn’t, you may need to request a plan amendment—especially if you’re in a leadership role or have influence over benefits.

2. Beware of Earnings on After-Tax Contributions

If you delay converting after-tax contributions, any earnings on those funds become taxable upon conversion. To avoid this, convert as soon as possible—ideally within the same tax year.

3. Pro-Rata Rule Doesn’t Apply (Usually)

Unlike the standard backdoor Roth, the Mega Backdoor Roth is generally not affected by the pro-rata rule—because the conversion happens within the 401(k) or from after-tax contributions with no pre-tax basis. However, consult a tax advisor to confirm your situation.

4. Timing Is Critical

Contributions and conversions should be done promptly. Some plans allow daily or weekly conversions; others only permit them quarterly. Know your plan’s rules.

Who Should Consider the Mega Backdoor Roth?

This strategy is ideal for:

- High earners making over $200,000 annually

- Individuals already maxing out their 401(k) and IRA

- Those with access to a flexible 401(k) plan

- People planning for long-term tax-free wealth transfer

- Professionals in high-tax states looking to reduce future tax burdens

If you’re in the top 10% of earners, this strategy could be one of the most impactful financial moves you make.

Key Takeaways

- The Mega Backdoor Roth allows high earners to contribute up to $46,000+ annually into a Roth IRA via their 401(k) plan.

- It requires a 401(k) plan that permits after-tax contributions and in-service Roth conversions.

- Contributions must be converted promptly to avoid taxable earnings.

- The strategy offers massive tax-free growth potential and no RMDs.

- It’s legal, IRS-compliant, and increasingly popular among affluent professionals.

FAQ

Is the Mega Backdoor Roth legal?

Yes. The Mega Backdoor Roth is fully compliant with IRS regulations. It uses existing rules for after-tax 401(k) contributions and Roth conversions. However, it depends on your employer’s plan allowing these features.

Can I do the Mega Backdoor Roth if my income exceeds the Roth IRA limits?

Absolutely. The Mega Backdoor Roth is specifically designed for high earners who are phased out of direct Roth IRA contributions. Since it operates through your 401(k), income limits don’t apply.

What happens if my 401(k) plan doesn’t allow after-tax contributions?

You cannot use the Mega Backdoor Roth unless your plan permits after-tax contributions and in-service Roth conversions. You may need to speak with HR or a financial advisor about amending the plan—especially if you’re in a position to influence benefits.

Final Thoughts: A Strategic Advantage for the Wealth-Building Elite

The Mega Backdoor Roth isn’t just another retirement tactic—it’s a wealth-building engine for high earners who want to maximize tax efficiency and long-term growth. While it requires careful execution and plan compatibility, the payoff is substantial: tens of thousands in annual tax-free contributions, decades of compounding, and a legacy of financial freedom.

If you’re serious about building generational wealth, this strategy deserves a top spot on your financial roadmap. Work with a qualified financial advisor or CPA to assess your plan’s features and implement the Mega Backdoor Roth correctly. The earlier you start, the greater the impact.